Complete Guide to FIP Transition in FY2026: Legal Procedures and Contract Practices for Solar Power Systems Over 50kW

✅ Key Takeaways

- 📌 From FY2026, solar power systems of 50kW or more will be eligible only for the FIP system; new FIT certifications will no longer be available

- ⚖️ Certification requirements have been significantly tightened, including mandatory resident explanation meetings and contractor supervision obligations, with immediate subsidy suspension risks for violations

- 🔍 Existing FIT projects must revise contracts and manage market price fluctuation risks when transitioning to FIP

- 💼 Explanation meeting obligations also apply to secondary transactions (business transfers, M&A), significantly impacting transaction practices

Table of Contents

Introduction

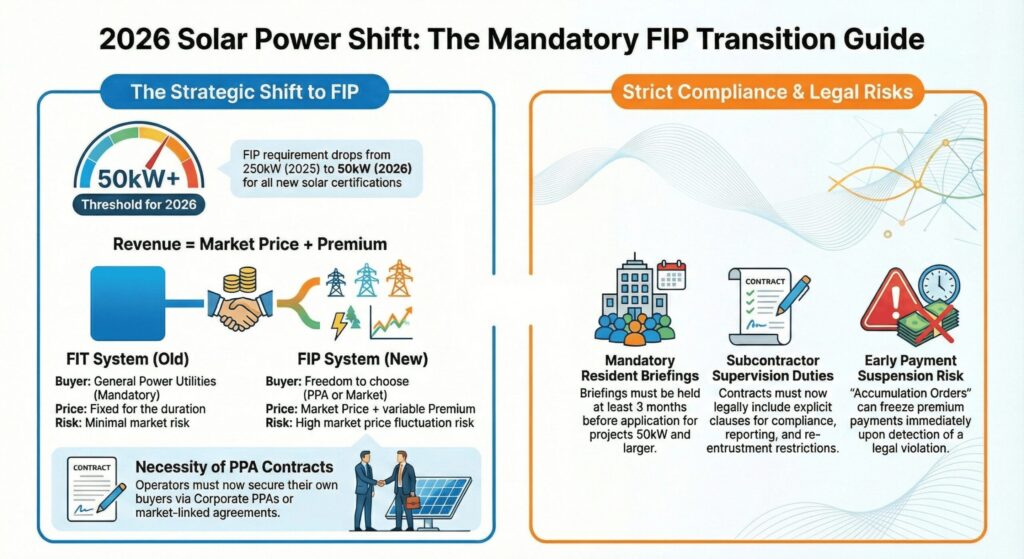

In this article, we will explain the transition to the FIP (Feed-in Premium) system from FY2026, focusing on legal procedures and contract practices. The FIP system, introduced in April 2022, has been gradually expanding, and FY2026 marks a major turning point. According to Ministry of Economy, Trade and Industry (METI) policy, facilities of 50kW or more will in principle only be eligible for the FIP system, and new certifications under the FIT system will no longer be accepted.

This transition has significant legal implications for business operators. This article provides practical guidance from a lawyer’s perspective on the legal procedures, contract revisions, risk management measures, and M&A considerations required for the FIP transition.

Legal Framework and Basic Structure

FIP System Overview and Legal Basis

The FIP system is based on the Renewable Energy Special Measures Act (for details, see METI policy PDF). The revenue structure differs significantly from FIT:

- FIT

Fixed-price purchase = Purchase price × electricity volume - FIP

Market sales + premium = (Market price + premium) × electricity volume

The premium is calculated as “benchmark price – reference price,” where the benchmark price is set by the Minister of Economy, Trade and Industry, and the reference price is based on JEPX spot market prices.

Differences from FIT System

Under FIT, electricity is purchased at a fixed price for a certain period regardless of market price fluctuations, with revenue guaranteed. In contrast, under FIP, business operators sell directly to the market while receiving premium payments. This means business operators bear market price fluctuation risks, requiring sophisticated risk management.

The FIP system allows the pursuit of higher revenues through market transactions while establishing a mechanism to secure stable income through premiums during low-price periods. Legally, transition from specified contracts to power purchase agreements (PPAs) is required, and contracts must incorporate terms regarding market linkage, imbalance risk allocation, and environmental value attribution.

Scope of FY2026 System Changes

Target Scope and Capacity Requirements

From FY2026, all solar power facilities of 50kW or more will be subject to the FIP system. Until FY2025, systems of 250kW or more were subject to FIP (METI materials), but the threshold has been lowered, bringing many rooftop solar and small-scale ground-mounted systems within scope. All systems eligible for business operator certification under the Renewable Energy Special Measures Act are subject, including:

- Ground-mounted systems

- Rooftop systems

- Agricultural solar (agrivoltaic) systems

- Parking lot solar systems

Mandatory Resident Explanation Meetings

Resident explanation meetings must be held at least three months before filing the FIT/FIP certification application. The target scope is “within 300 meters” for systems under 2,000kW, and “within 1 kilometer” for systems of 2,000kW or more. For systems under 50kW, prior notification measures such as posting flyers can substitute.

Explanation content must be clear regarding:

- Installation location and facility scale

- Environmental impact (noise, glare, water runoff management)

- Management system and emergency response

- Post-operation decommissioning plans

Meeting records must be properly created and submitted with the certification application. Omitting explanation meetings or providing inadequate explanations can result in denial of new certification or revocation of existing certification.

Required Permits (Forest Law, Development Act, etc.)

The revised Renewable Energy Special Measures Act, effective October 1, 2023, requires obtaining necessary permits before certification, including:

- Forest Law (development permits in forest areas)

- Act on Prevention of Disaster Caused by Steep Slope Land Collapse

- Sediment Control Act and other sand control laws

- Urban Planning Act (development permits)

Previously, permits could be obtained after certification, but now they are prerequisites. If permits cannot be obtained within three years of certification, the certification may be revoked. Business operators must work with experts to identify and secure required permits early in the project.

Contract Practices for FIT-to-FIP Transition

Application for Amendment and Contract Termination

Existing FIT-certified operators who wish to transition to FIP must file an amendment application with the Agency for Natural Resources and Energy. After approval, the existing specified contract must be terminated and replaced with a market-linked contract.

The transition procedures are legally stipulated as follows:

- Amendment Application: File FIP conversion application through the electronic application system

- Specified Contract Termination: Notify the transmission and distribution operator of contract termination

- New Contract Execution: Conclude PPA or direct market trading contract

- Adjustment of Imbalance Reduction Plan: Review supply forecasting accuracy and update the plan

These procedures involve detailed legal requirements, making advance consultation with lawyers and electric power transaction experts advisable.

Types of Contracts and Key Provisions

When transitioning from FIT to FIP, business operators can choose from several contract types, each with different contract terms and legal risk allocation:

Market-Linked PPA: Pricing linked to JEPX market prices; price fluctuation risk is high but enables pursuit of high revenues during high-price periods. Contracts must clearly define:

- Price determination mechanism (index, calculation period, settlement method)

- Environmental value attribution (renewable energy certificates, non-fossil certificates)

- Imbalance risk allocation (cost sharing between seller and buyer)

- Output curtailment response (compensation or no compensation)

- Contract period and renewal conditions

Fixed-Price PPA: Pricing negotiated with specific buyers at fixed rates; revenue is more stable than market-linked but typically at lower price levels. Contracts require clear definition of:

- Fixed price levels and duration

- Price revision clauses (based on consumer price index, etc.)

- Credit risk (buyer’s financial soundness assessment and guarantees)

- Default response (payment delays, buyer bankruptcy, etc.)

Direct Market Trading: Business operators directly participate in JEPX spot and intraday markets; requires advanced market operation capabilities and bears all price fluctuation and imbalance risks. This requires:

- JEPX membership and trading system

- Advanced forecasting and trading systems

- Balancing group or retail electricity provider arrangements

Impact on Existing Financing and Collateral

FIT-to-FIP transition significantly impacts existing project financing and collateral arrangements. Under FIT, specified contracts guaranteed fixed revenues, serving as primary collateral. Under FIP, market price fluctuations introduce revenue uncertainty, requiring financing contract revisions:

- Reassessment of Collateral Value: Transition to FIP may reduce specified contract collateral value, requiring additional collateral or guarantees

- Prior Consent Clauses: Many financing contracts require lender consent for business plan changes; FIT-to-FIP transition typically requires such consent

- Reassessment of Financial Covenants: Debt service coverage ratio (DSCR) and other financial indicators must be recalculated based on FIP revenue forecasts

Neglecting advance negotiation with financial institutions can result in covenant violations or demands for early repayment, making early disclosure and coordination essential.

Considerations for Secondary Transactions

Explanation Obligations in Business and Share Transfers

When transferring FIP/FIT-certified businesses or shares in certified companies, explanation meeting or prior notification obligations apply to the acquirer as well. Specifically:

- If the acquired business did not hold explanation meetings before initial certification, the acquirer must conduct them

- If a new explanation meeting is required due to significant plan changes, the acquirer must hold it

These explanation obligations directly impact transaction execution, requiring schedule adjustments and information disclosure during due diligence.

Key Provisions in M&A Agreements

The following provisions should be incorporated into M&A agreements (share purchase agreements, asset purchase agreements) related to FIP businesses:

Conditions Precedent:

- “Explanation meetings have been properly held and no major objections from residents remain”

- “FIP certification has been validly obtained and no risk of revocation exists”

- “Required permits (forest law, development permits, etc.) have been obtained and remain valid”

Representations and Warranties (seller representations):

- “There are no disputes or litigation risks with residents or local governments”

- “Contractor management has been properly conducted and contractors meet legal requirements”

- “No violations of the Renewable Energy Special Measures Act or related laws and regulations exist, and no administrative guidance has been received”

Covenants (seller post-closing obligations):

- “Cooperate in explanation meetings or prior notifications if required”

- “Maintain contractor management systems and ensure smooth transition”

- “Secure necessary consents from financial institutions and PPA counterparties”

Indemnification and Liability Caps: Allocate liability for breach of representations and warranties; specify indemnification scope (legal costs, administrative penalties, resident compensation) and caps.

These provisions are essential for protecting acquirers from legal risks while enabling smooth transaction execution.

Contractor Supervision Obligations and Required Contract Provisions

Scope of Supervision Obligations and Legal Basis

Article 10-3 of the revised Renewable Energy Special Measures Act imposes supervision obligations on certified operators over all contractors and subcontractors involved in:

- Design operations

- Construction work

- Operation and maintenance (O&M)

- Other outsourced operations

When contractors or subcontractors commit legal violations (illegal forest development, permit violations, safety regulation breaches), certified operators are held accountable. Accumulation orders or certification revocation may result regardless of whether the certified operator was directly involved.

Required Contract Clauses

To fulfill supervision obligations, contracts with all contractors must clearly include the following provisions:

Legal Compliance Clauses:

- “The contractor shall comply with all applicable laws and regulations, including the Renewable Energy Special Measures Act, forest law, and safety regulations”

- “If administrative guidance or corrective orders are received, the contractor must immediately report to the business operator and promptly implement improvements”

Reporting Obligations (including photographic evidence):

- “The contractor shall submit monthly reports detailing work progress, permit status, and safety measures”

- “Reports must include on-site photographs and proof of permit acquisition”

- “If abnormalities or risks are discovered, immediate reporting is required regardless of scheduled reporting dates”

Restrictions on Re-subcontracting:

- “Re-subcontracting requires prior written approval from the business operator”

- “When re-subcontracting, the contractor shall ensure the re-subcontractor meets the same legal compliance and supervision standards”

Termination for Breach:

- “If the contractor violates this contract or applicable laws and fails to remedy the violation within a specified period after notice, the business operator may immediately terminate this contract”

- “Upon termination, the contractor shall bear all losses and damages incurred by the business operator”

These provisions are essential for mitigating legal risks to certified operators and demonstrating fulfillment of supervision obligations to administrative authorities.

Accumulation and Repayment Order Risks

Overview of Accumulation Order System

When certified operators violate the Renewable Energy Special Measures Act or fail to fulfill contractor supervision obligations, the Minister of Economy, Trade and Industry may immediately issue an “accumulation order” to suspend FIT/FIP subsidy payments. No prior hearing is required, and orders can be issued swiftly.

Under accumulation orders:

- Transmission and distribution operators withhold FIP premium or FIT purchase price payments

- Withheld amounts are held by operators until violations are remedied

- If violations remain unremedied, “repayment orders” may be issued, requiring return of accumulated funds to the national treasury

For FIT, the accumulated amount equals “purchase cost minus avoidable market revenue”; for FIP, the full premium amount is accumulated. Amounts can be substantial, posing significant financial risk to business operations.

Legal Risks and Case Studies

Typical scenarios triggering accumulation orders include:

- Failure to obtain required permits (forest law violations, unauthorized development)

- Resident explanation meeting omissions or inadequate explanations

- Contractor violations (safety standard breaches, illegal disposal)

- Facility management violations (inspection omissions, failure to implement required safety measures)

In severe cases, certification may be revoked before repayment orders are issued, permanently halting business operations. Several cases have been reported of certifications being revoked due to illegal forest development or violation of resident agreement terms.

Preventive Measures and Risk Management

To prevent accumulation and repayment orders, the following risk management measures are essential:

Compliance System Development:

- Establish internal rules for legal compliance

- Appoint compliance officers and conduct periodic training

- Conduct internal audits and inspections

Contractor Selection and Monitoring:

- Verify contractor legal compliance records and technical capabilities before selection

- Implement periodic inspections and audits

- Mandate monthly reporting including photographic evidence

- Conduct unannounced site inspections as needed

Early Detection and Remediation Processes:

- Establish and publicize internal reporting (whistleblowing) channels

- Investigate reports and suspected violations immediately and implement remedial measures

- Report to administrative authorities early and cooperate on improvement plans

These measures not only prevent accumulation orders but also demonstrate good faith compliance to administrative authorities, potentially mitigating penalties.

Practical Roadmap

Schedule and Checklist for New Certifications

When applying for new FIP certification from FY2026, business operators should follow this timeline:

9 Months Before Application: Project planning phase

- Site selection and development feasibility study

- Identification of required permits (forest law, development act, sediment control act)

- Assessment of grid connection feasibility and consultation with transmission and distribution operators

- Engagement of lawyers and consultants

6 Months Before Application: Permit acquisition phase

- Filing applications for forest law, development permits, etc.

- Advance consultation with local governments and adjustment of plans

- Preparation of explanation meeting materials and determination of target residents

3 Months Before Application: Explanation meeting phase

- Notification to residents and scheduling of explanation meetings

- Holding explanation meetings and creating records

- Addressing resident concerns and revising plans as necessary

- Ensuring all permits are obtained

At Application: Certification application and grid connection

- Filing FIP certification application through electronic system

- Application for grid connection agreement with transmission and distribution operators

- Submission of financing and insurance arrangements

- Submission of contractor management plans

Post-Certification: Contract execution and construction commencement

- Execution of PPA or direct market trading contracts

- Execution of financing agreements and establishment of collateral

- Execution of contractor agreements (incorporating supervision clauses)

- Construction commencement and periodic reporting

This roadmap enables smooth certification acquisition while managing legal risks.

Procedures for Existing FIT Project Transitions

For existing FIT-certified projects transitioning to FIP, the following phased approach is recommended:

Phase 1: Economic Assessment

- Revenue simulation under FIP (multiple scenarios based on JEPX market price forecasts)

- Comparison with continued FIT revenue and break-even analysis

- Assessment of financing and tax impacts

- Determination of transition feasibility

Phase 2: Contract Organization

- Review of existing specified contracts and financing agreements

- Identification of required consents and approvals

- PPA negotiation (selection of market-linked or fixed-price types)

- Coordination with financial institutions and re-negotiation of financing terms

Phase 3: Legal Procedures

- Filing of FIP conversion amendment application

- Holding of resident explanation meetings (if required)

- Confirmation of permit validity and acquisition of additional permits as needed

- Notification of specified contract termination

Phase 4: Transition Implementation

- Execution of new PPA

- Adjustment of imbalance reduction plan

- Implementation of new revenue management and accounting systems

- Operational staff training and manual updates

Early initiation of this process is advisable, as coordination with financial institutions and PPA negotiations can be time-consuming.

M&A Due Diligence Items

In M&A transactions involving FIP businesses, the following due diligence items are essential:

Legal Due Diligence:

- Validity of FIP certification (certification documents, amendment history, administrative guidance records)

- Status of explanation meetings (records, resident feedback, outstanding issues)

- Permit status (forest law, development permits, grid connection agreements)

- Litigation and dispute risks (resident disputes, administrative proceedings, environmental issues)

Contract Due Diligence:

- PPA terms (pricing, contract period, termination conditions, environmental value)

- Contractor agreements (compliance clauses, supervision provisions, performance bonds)

- Financing agreements (consent requirements, collateral, covenants, default events)

- Insurance arrangements (coverage, exclusions, premium payment status)

Financial Due Diligence:

- Revenue trends (market sales, premium income, feed-in tariff comparison)

- Cost structure (O&M costs, grid usage fees, imbalance costs)

- Debt status (loan balances, repayment schedules, interest rates)

- Cash flow forecasts and financial covenant compliance

Technical Due Diligence:

- Facility condition and maintenance records

- Power generation performance and comparison with forecasts

- Grid compliance and curtailment history

- Remaining useful life and major repair plans

Based on this due diligence, transaction prices, representations and warranties, and indemnification provisions should be structured. Particularly, explanation meeting obligations and accumulation order risks should be carefully assessed and contractually addressed.

When to Consult a Lawyer

Navigating the FIP transition requires specialized legal expertise in multiple areas. Key consultation timings include:

Project Startup Phase

- Design of explanation meeting process and preparation of resident response strategies

- Drafting of PPA contracts and review of key terms

- Structuring of financing and establishment of collateral arrangements

- Identification of required permits and preparation of application strategies

Early legal involvement from the project planning stage reduces subsequent trouble and enables smooth certification acquisition.

During Ongoing Operations

- Review of contractor agreements and enhancement of supervision provisions

- Development of legal compliance systems and internal audit implementation

- Response to resident complaints and negotiation strategies

- Addressing administrative guidance and preparing improvement reports

Even after operations commence, periodic legal checks are essential for risk management.

Trouble Response Phase

- Response to accumulation orders and preparation of remediation plans

- Defense against certification revocation proceedings

- Litigation with residents or contractors

- Response to breach of financing covenants

When legal problems arise, early lawyer involvement is critical for damage minimization and swift resolution.

M&A and Refinancing Phase

- M&A due diligence and risk assessment

- Drafting of transaction agreements and negotiation support

- Refinancing structuring and lender negotiations

- Review of contractor transitions and consent procedures

Complex legal structuring is required in M&A and refinancing, making lawyer involvement indispensable.

Summary

The transition to the FIP system in FY2026 represents a major turning point for the solar power industry. First, the shift from FIT to FIP imposes market price fluctuation risks on business operators, requiring sophisticated risk management. Additionally, tightened certification requirements—including mandatory explanation meetings and contractor supervision obligations—demand meticulous legal compliance. Furthermore, in secondary transactions such as M&A, explanation obligations and legal due diligence become more complex, necessitating careful contractual structuring. Finally, the new accumulation and repayment order systems pose significant financial risks, making preventive legal risk management essential.

Having supported numerous solar power businesses, I recognize that successful FIP transitions require early legal checks, strategic contract design, and robust compliance systems. Rather than adopting a “wait-and-see” approach, proactive preparation is key to sustainable business operations.

We encourage business operators to consult legal experts early to navigate the FIP transition smoothly while ensuring legal compliance and pursuing business growth.

- Low-Voltage Solar Power Legal Practice 2025-2026: Latest Trends in Development and Secondary Market Transactions for Lawyers - Subsidy Suspension Risks

- [Column Writing]【ESG Strategies for Business】Vol. 29 Protection of Foreign Workers and Countermeasures Against Forced Labor (1): International Regulations and Malaysia’s Response

関連記事

-

[Column Writing]【Kin’yū Hōmu Jijō】No. 2276 Settlement in Southeast Asia and Aging Business Leaders

[Column Writing]【Kin’yū Hōmu Jijō】No. 2276 Settlement in Southeast Asia and Aging Business Leaders -

[Column Writing]【ESG Strategies for Business】Vol. 29 Protection of Foreign Workers and Countermeasures Against Forced Labor (1): International Regulations and Malaysia’s Response

-

Low-Voltage Solar Power Legal Practice 2025-2026: Latest Trends in Development and Secondary Market Transactions for Lawyers – Subsidy Suspension Risks

-

Japan’s Megasolar Countermeasure Package: A Lawyer’s Comprehensive Analysis — The True Nature of the “Predetermined Course” and Seven Key Legal Issues from a Developer’s Perspective

-

Indonesia Tightens Corporate Procedures: Practical Implications of MOL Regulation 49/2025

-

2026: A Historic Turning Point in Japan’s Energy Policy – A Comprehensive Guide to Seven Major System Changes Affecting Businesses

-

Legal Issues in Sustainable Finance for 2026: Transition Finance and Green Bond Practice

-

[Column] How to Make Effective Lawyer Requests: Information Sharing Determines Success